Medicare Advantage vs. Medigap:

Which Plan is Right for You?

Medicare in 2025 is seeing several key changes, including expanded Medicare Advantage options and updates to prescription drug coverage. If you've noticed more TV ads about Medicare Supplements and Medicare Advantage, it's because these programs continue to grow, including right here in Brooksville, Florida.

There's also been some confusion around terms like "Trump Care" and other misleading phrases. We're here to clear things up and make Medicare easy to understand.

Medicare Advantage vs. Medigap

TV ads about Medicare Supplements and Medicare Advantage are everywhere right now. This year, Medicare Advantage programs are expanding significantly in many areas, including here in Brooksville, Florida.

There’s also a lot of talk about terms like “Trump Care” and other misleading phrases. Let’s clear up the confusion.

Have You Seen the Ads and TV Commercials?

You’ve probably seen Joe Namath on TV saying, “I called the Medicare Coverage Helpline, and they instantly looked up my coverage.” This ad has been running for years, and many people call us with questions about it.

You might have also noticed Dr. Phil or Dr. Oz talking about Medicare Advantage. But do you know what they really mean?

These are paid ads promoting Medicare plans. While they may mention real benefits, it’s important to understand what’s being advertised and whether it’s the right fit for you.

There’s No One-Size-Fits-All Medicare Plan

Medicare Advantage and Medigap (Medicare Supplement) work differently, and many of our customers prefer one over the other. We’re not here to tell you which to pick—we just want to explain the differences so you can decide what’s best for you.

Some people only have one option available, so the choice is easy. Others may choose based on cost—one plan might have lower premiums, while the other helps reduce out-of-pocket expenses. If you can afford a slightly higher premium, you might get more benefits.

Let’s go over the details together so you can make the right choice.

Medicare Advantage plans are private insurance options that cover everything Original Medicare does. Many also include extras like dental, vision, hearing, and wellness programs, but the details depend on the plan.

In general, Medicare Advantage plans offer more benefits than downsides, but it’s important to understand how they work to see if they’re right for you.

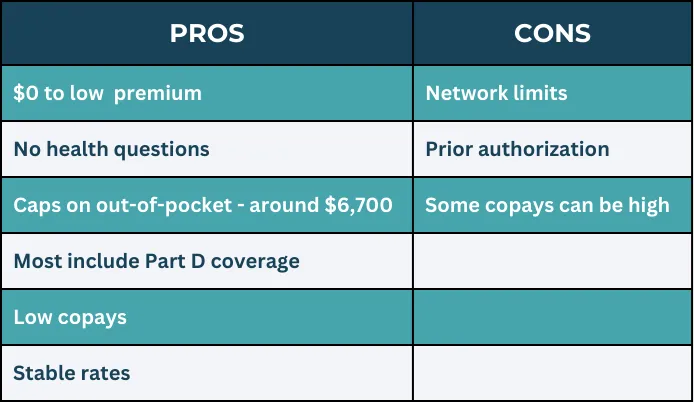

The Pros Explained

Medicare Advantage plans usually cost less in monthly premiums, no matter your health condition.

In the past, the only health question asked was about end-stage renal disease, but starting this fall, even that question is gone.

Most plans also include prescription drug coverage (Part D) at no extra cost. Plus, rates tend to stay steady across the country with little change.

The Cons Explained

One downside of Medicare Advantage is that you may have to use certain doctors and hospitals, meaning you might not be able to see your preferred provider.

Another issue is prior authorization, your doctor may need approval from the plan before ordering certain tests or treatments, which can be inconvenient.

Costs can also add up. For example, hospital stays may have daily copays, and outpatient surgery fees often range from $200 to $350, depending on the plan. Over time, these expenses can become a burden.

Medicare + Medigap: Pros and Cons

A Medigap plan (also called a Medicare Supplement) helps cover costs that Original Medicare doesn’t, like copays, coinsurance, and deductibles.

There are different Medigap plans, such as F, G, K, L, and N, and each one covers different expenses. Your choice will depend on the coverage you need.

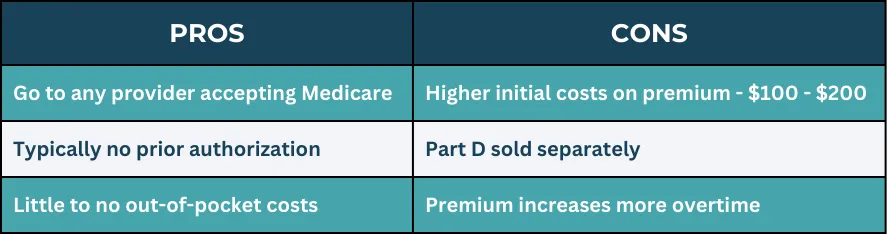

The Pros of Medigap

● See Almost Any Doctor – Medigap lets you visit any doctor or hospital that accepts Medicare—about 97% nationwide.

● No Prior Authorization – Medicare usually approves tests without extra approval, making things easier compared to Medicare Advantage.

● Low Out-of-Pocket Costs – If you had Medicare before January 1, 2020, you may still have Plan F, which covers all medical costs. For 2025, Plan G’s only out-of-pocket cost is the Part B deductible, which is now $240 per year.

Many people love the freedom and coverage Medigap offers, but it’s also important to consider the downsides.

The Cons of Medigap in 2025

● Higher Monthly Cost – Medigap premiums in 2025 typically range from $110 to $220 per month and may increase over time. A 65-year-old woman might start at around $95 per month, depending on the plan and location.

● Separate Drug Coverage – Medigap doesn’t include prescription drug coverage (Part D), so you’ll need to buy a separate plan, which can cost $15 to $85 per month, depending on your medications and pharmacy.

● Health Questions for Approval – To get a Medigap plan at a lower rate (or even qualify at all), you may have to answer health questions. This process, called medical underwriting, can make it harder to switch plans as you age or develop health conditions.

While Medigap offers great coverage and flexibility, these factors are important to keep in mind.

It’s Hard to Decide on a Plan. So Work with Us

Picking the right plan isn’t easy—it depends on your health, budget, and coverage needs.

That’s why it helps to talk to experts. At MAC Insurance, our team can compare all your options and find the best fit for you—at no cost.

We treat our clients like family and only recommend plans we’d choose for our own loved ones. Call us today at 352-652-4100. We’re happy to help!

Medicare Explained

Want more help understanding

MEDICARE ADVANTAGE VS MEDIGAP

Trying to decide between Medicare Advantage and Medigap (Medicare Supplement)? At MAC Insurance, we make it easy to understand the differences and choose the best option for your needs—at no cost to you.

Our licensed experts will walk you through Medicare Advantage plans, Medigap options, and prescription drug coverage (Part D) so you can make an informed decision with confidence.

Call us today at 352-652-4100 or send us an email—let’s find the right Medicare plan together!

ADDITIONAL QUESTIONS TO BE ADVISED ON:

Will my preferred doctors and hospitals accept this plan?

Whether your doctor accepts a plan depends on the type you choose. Medicare Advantage has networks, so you may need to use specific doctors and hospitals, while Medigap (Medicare Supplement) lets you see any provider that accepts Medicare—about 97% nationwide. If keeping your doctor is important, we can check which plans they accept.

Do I need referrals to see specialists?

It depends on the plan you choose. Medicare Advantage HMO plans usually require a referral to see a specialist, while PPO plans typically do not. Medigap (Medicare Supplement) plans follow Original Medicare rules, meaning you can see any specialist who accepts Medicare without a referral.

How much will I pay in out-of-pocket costs, such as copays and deductibles?

With Medicare Advantage, you may pay low or $0 premiums but have copays, deductibles, and an out-of-pocket maximum each year. With Medigap, you’ll pay a higher monthly premium but have lower out-of-pocket costs for medical care.

Is there a cap on annual expenses?

Medicare Advantage plans have an annual out-of-pocket maximum, which limits how much you pay each year for covered services. Medigap plans don’t have a cap, but they help cover Medicare’s costs, so your expenses stay low.

Does the plan include Part D (prescription drug coverage), or will I need a separate plan?

Medicare Advantage plans often include Part D (prescription drug coverage). Medigap plans do not include drug coverage, so you’ll need to buy a separate Part D plan.

Are my medications covered, and what will they cost?

Medicare Advantage plans with Part D and standalone Part D plans each have a drug list (formulary) that shows which medications are covered and how much they cost. Prices vary by plan, pharmacy, and drug tier.

How does each plan handle medical emergencies when traveling?

Medicare Advantage plans usually cover emergencies within the U.S., but coverage outside the country is limited. Medigap plans often include emergency coverage abroad, helping pay for urgent care outside the U.S.

Why was Medicare established?

Medicare was created to offer healthcare benefits to retirees. Before its introduction, retirees who lost employer-sponsored coverage had few health insurance options.

How can I check if I'm enrolled in Original Medicare?

To see if you're enrolled in Original Medicare, check your Social Security check deductions. If you're receiving Social Security benefits, you're automatically enrolled at 65, and Medicare premiums are deducted from your benefits. You can also verify your enrollment online at MyMedicare.gov or by calling the Social Security Administration.

At what age can I get Medicare?

People receiving disability benefits for 24 months qualify for Medicare at any age, as do those with ESRD or ALS. Otherwise, Medicare eligibility begins at 65.

Who does not qualify for Medicare?

To qualify for Medicare, individuals must be U.S. citizens or have lived in the U.S. for at least five years. Those under 65 without disabilities, ESRD, or ALS are not eligible.

What documents are required for a Medicare application?

You must provide proof of U.S. citizenship or legal residency, along with your birth certificate and driver's license.

Do I need a primary care physician for Medicare?

No, you don't need to select a primary care physician with Original Medicare. However, choosing providers who accept Medicare assignment can help minimize your out-of-pocket costs.

Do I have to get a referral to see a specialist if I’m on Medicare?

No, you don’t need a referral to see a specialist. However, your out-of-pocket costs will be lower if you choose a specialist that accepts Medicare assignment.

Family-Owned. Relationship-Driven.

Medicare & Health Insurance Made Simple.

806 W Dr. M L King Jr Blvd,

Brooksville, FL

34601

Phone Number

(352)-652- 4100

EXPLORE OUR SERVICES

TRUSTED AND RECOGNIZED

LET'S STAY CONNECTED!

📩 Contact us today and let us represent you for FREE!

We are not connected with or endorsed by the United States government or the federal Medicare program. We do not offer every plan available in your area, and any information we provide is limited to those plans we do offer in your area. Please get in touch with Medicare.gov or 1-800-MEDICARE to get information on all your options.

Copyright © 2026 MAC Insurance. All rights reserved.